⏱ Estimated reading time: 3 min read

The U.S. federal tax system applies different taxes to various types of income, primarily ordinary income, self-employment, and the net investment income taxes (NIIT).

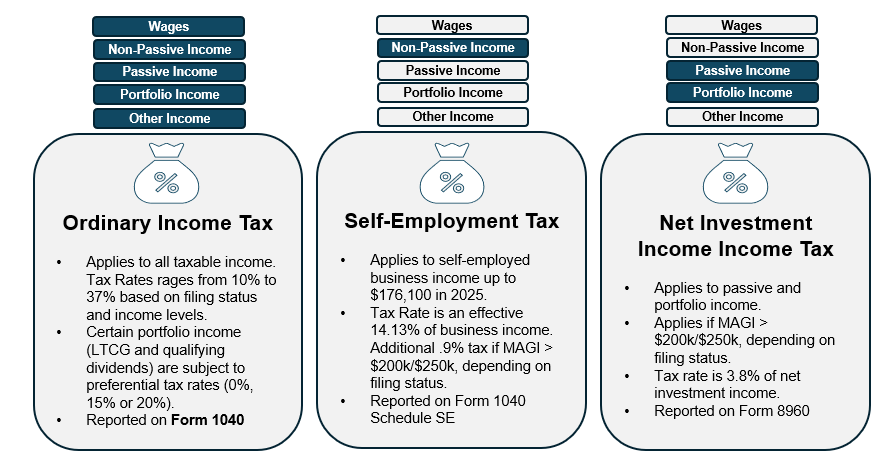

Ordinary income tax applies broadly to wages, business profits, and most other types of earned income, with rates for the 2025 tax year ranging from 10% to 37%, depending on your filing status and income level. This tax applies whether the income is active passive (investment or limited involvement) or you materially participate (e.g., general partner in a partnership).

Self-employment tax applies only to non-passive business income—that is, income from a trade or business where you materially participate (e.g., a sole proprietorship, LLC, or partnership where you’re actively involved). The combined rate is 15.3%: 12.4% for Social Security (up to the annual limit) and 2.9% for Medicare, with an additional 0.9% surtax on income above $200,000 (single) or $250,000 (married filing jointly). This is in addition to ordinary income tax and is not applied to passive income or portfolio income.

Net Investment Income Tax (NIIT), on the other hand, applies to passive and portfolio income, such as dividends, interest, capital gains, rental income, and business income where the taxpayer does not materially participate (e.g. limited partnership interest). The rate is 3.8% and is assessed on the lesser of (1) net investment income or (2) the excess of modified adjusted gross income (MAGI) over $200,000 (single) or $250,000 (married filing jointly). Importantly, NIIT does not apply to wages or active business income.

Conclusion

Understanding whether income is passive or non-passive is crucial because it determines whether you’re subject to self-employment tax or NIIT, in addition to ordinary income tax. For example, a real estate investor who does not materially participate may owe income tax and NIIT on rental income, while a self-employed consultant would owe income tax and self-employment tax on their earnings. Strategic planning—such as entity structure considerations, material participation and documentation, or investment timing—can help reduce exposure across these layers of taxation.

Disclaimer: The information provided herein is intended solely for informational purposes and no person(s) or other third-party may rely upon it as financial, tax, or legal advice or use it for any other purposes. As a result, Royal Financial, and any affiliates, assume no responsibility whatsoever to readers, or any other persons for that matter, as a result of the information contained herein.