⏱ Estimated reading time: 6 min read

With interest rates expected to fall over the next few months, many home & auto-owners are asking: Should I refinance? Before deciding, here’s what you need to know:

- How “Fed Rate Cuts” directly and indirectly impact consumers;

- What refinancing is;

- Options available (will vary by provider); and

- When it makes sense; and

- The process and costs (documentation, timeline, etc.)

1. How Federal Reserve rate cuts directly and indirectly impact consumers

When the Federal Reserve cuts interest rates, it’s specifically cutting the “Fed Funds Rate”. The Fed Funds Rate is the interest rate at which commercial banks lend each other funds overnight (i.e. short-term). Not all borrowing costs react the same way to the “Fed Funds Rate”. Here’s the breakdown:

A. Directly Impacted: Credit cards, HELOCs, and other variable-rate debt

- These are tied to the prime rate, which moves almost immediately after the Fed changes the federal funds rate.

- Expect to see lower interest charges on revolving credit within one or two billing cycles.

The Prime Rate (~7.25% as of Sept 2025) is a benchmark lenders use for top borrowers and as a baseline for many loans, including credit cards, personal loans, and mortgages.

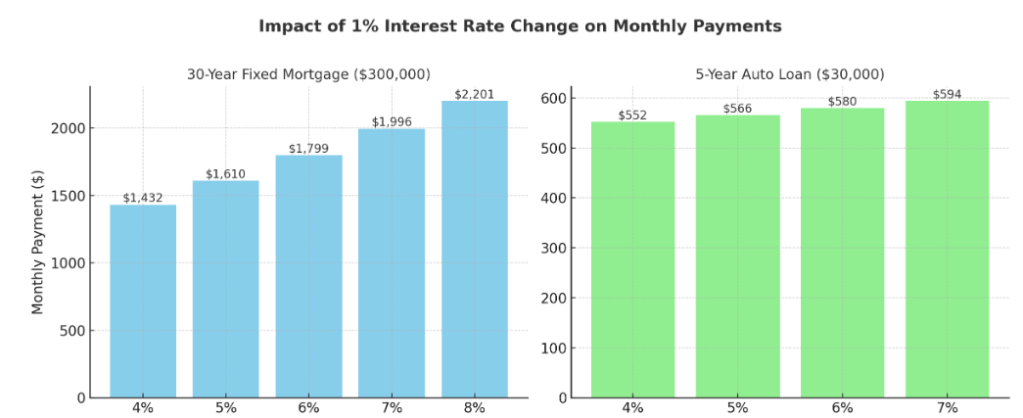

B. Indirectly Impacted: Mortgage rates (30-year, 15-year fixed) and Auto Loans

- Mortgages: Mortgage rates have historically follow the 10-year Treasury yield more than the Fed funds rate.

- Auto loans: Auto lenders price loans off broader credit markets, not just the Fed funds rate. As borrowing costs drop in the economy, auto loan rates tend to drift lower, but usually not as sharply or immediately as credit card rates.

Fed cuts can influence Treasury yields, which affect mortgage rates, but the link isn’t exact. Mortgage rates may lag, move differently, or even drop before Fed cuts — as seen in 2025 amid the real estate slowdown.

2. What is refinancing?

Refinancing means replacing your current mortgage with a new one — usually with better terms. Think of it as “trading in” your loan. You still own your home, but you get a new loan that pays off the old one. The actual mechanics here, will depend on the refinancing option you choose.

3. Refinancing options

Depending on the lender, you may have various refinancing options. Below are a few of the typical options provided. It’s important to confirm the options with your particular lender.

- Rater and Term Refinance (most common): Swap into a lower rate and/or different loan length.

- Cash-out Refinance: Tap equity for cash, increasing loan balance. Can be used for home renovations, repairs, etc.

- Cash-in Refinance: Put up additional cash to lower balance, rate, and / or eliminate PMI.

- Streamline refinance: Easier, less paperwork, and for FHA / VA / USDA loans.

4. When does refinancing make sense?

When deciding whether refinancing makes sense, at minimum, you should ask your self the following 3 questions:

- Will the monthly savings outweigh the closing costs?

- Do you plan on staying in the home long enough to benefit?

- Does refinancing help you reach other financial goals (e.g. lower payment, faster pay-off, cash for projects, etc.)?

Your lender can show how refinancing affects your rate, term, payment, and balance, while your accountant or advisor can fit those numbers into your budget and financial plan

Royal Financial Planning View: Ask your banker “If I refinance at the lower rate but keep my term the same, what are my monthly savings after closing costs?”. That amount represents net savings from rate changes alone. If affordable, keep paying your old (higher) amount to pay down the loan faster or set aside funds for future payments in case you are worried about your job or thinking of switching jobs.

5. The process and costs

On average, a mortgage refinance takes 30–45 days from application to closing, while an auto loan refinance usually takes just a few days to a week. The table below shows the typical timeline and documentation for each.

| Loan Type | Typical Timeline | Documentation Needed |

|---|---|---|

| Mortgage Refinance | 30–45 days | – Government-issued ID – Pay stubs, W-2s, last 2 years’ tax returns – Bank / investment account statements – Current mortgage statement – Homeowner’s insurance, property tax bill – Appraisal & title insurance |

| Auto Loan Refinance | Few days – 1 week | – Government-issued ID – Proof of income (pay stubs/tax return) – Vehicle registration, VIN, mileage – Proof of insurance – Current loan statement |

With respect to costs, mortgages have significant closing costs while auto loan refinancing is usually cheaper. The table below shows the typical costs for each.

| Type of Loan | Typical Closing Costs / Fees | As % of Loan Balance / Typical Amount | Key Fee Components Included / Notes |

|---|---|---|---|

| Mortgage Refinance | Between 2% – 6% of the new loan principal depending on your state and lender . | If loan = $200,000 → closing costs might be $4,000 to $12,000 | Appraisal, credit check, title search & insurance, origination fee, points, recording & attorney fees, survey (if needed). |

| “Typical Avg by State / Smaller Loans” Mortgage | Lower percentages when excluding heavy tax / recording / state-specific costs | Example: national average ~ 0.7–1.5% in states without large fees; e.g. $2,400 for avg refinance ($340k loan) = ~0.72% . | Excludes heavy state/local taxes, large title or survey fees; location matters a lot. |

| Auto Loan Refinance | Usually small fixed fees rather than large % fees. | Common auto-refi cost: $0-$300 total (title transfer, registration, application). | Might include early payoff / prepayment penalty, title & registration fees, processing/application fees, sometimes lien handling fees. |

Conclusion

With rates poised to drop, now is the perfect time to explore refinancing and getting your ducks (documentation) in order. But it’s not a one-size-fits-all decision. Run the numbers, weigh your goals, and talk to your mortgage banker and accountant.

Click mortgage or auto loan to view our respective calculators.

Disclaimer: The information provided herein is intended solely for informational purposes and no person(s) or other third-party may rely upon it as financial, tax, or legal advice or use it for any other purposes. As a result, Royal Financial, and any affiliates, assume no responsibility whatsoever to readers, or any other persons for that matter, as a result of the information contained herein.