⏱ Estimated reading time: 6 min read

The IRS is especially skeptical when a taxpayer shows repetitive losses over multiple years without making any changes to improve profitability – this is one of the strongest indicators of hobby activity.

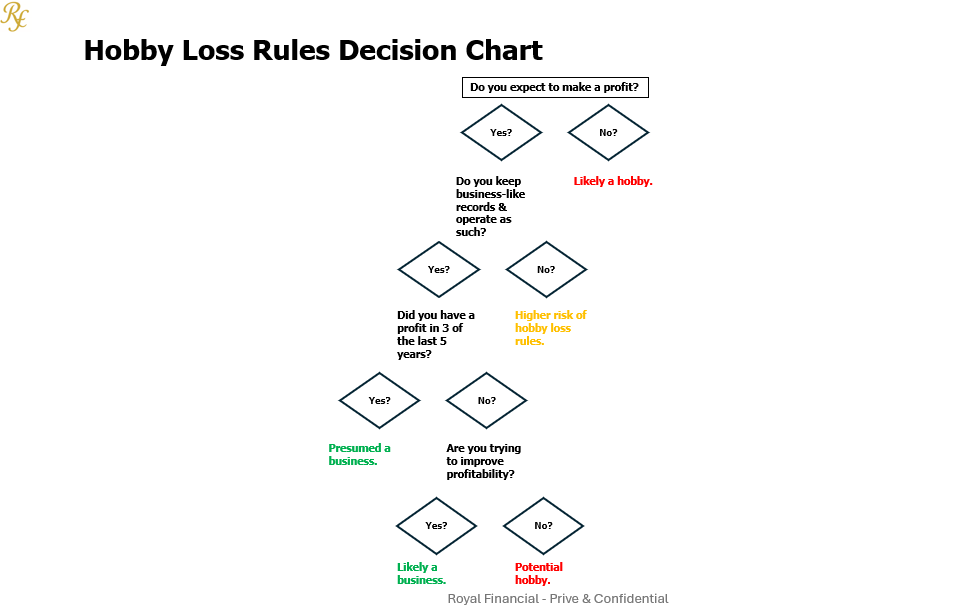

With that said, if you are incurring repeated losses, it would be important to understand the distinction between the IRS treating your activity as a hobby vs. a business. This can be done through an IRS audit or a routine year-end review.

It’s important to note here that “gig workers” (e.g., Uber, DooraDash, Instacart, etc.) are almost never considered hobbies because (1) the activity involves clear compensation for services (2) taxpayers enter into commercial arrangements with platforms and (3) the intent to earn a profit is inherent. Therefore, the hobby-loss rules can apply to some “side hustles”, but not the ones where taxpayers are being paid for a service in a structured marketplace.

Why the distinction matters? The distinctions between a hobby & a business are important because it dictates where on the tax return the activities are reported, what is reported, and how they are taxed.

A “hobby” is something done for pleasure or recreation rather than with the intent to earn a profit. Examples include arts/crafts; breeding/training of animals; collectible reselling; photography unrelated to commercial clients; amateur sports activities, and YouTubing/streaming with minimal or no monetization history. For tax purposes you are not permitted to deduct any expenses other than COGS in the determination of hobby taxable income. Furthermore, COGS, can’t reduce income below $0. These items of income are reported on Schedule I Part I Line 8j of the individuals Form 1040.

A “business” is entered into with a genuine profit motive. For tax purposes, taxpayers may deduct all expenses, not just COGS, generated in the ordinary course of the business, even if it generates a net tax loss that can be used to offset other wage income. These items of income & expense are typically reported on Schedule C & Schedule SE of the individual’s Form 1040 (unless reported on a business return).

Although you can’t deduct expenses, other than COGS, in determining hobby income, on the plus side hobby related income isn’t subject to self-employment taxes (effectively ~14.13% of your business profit on Schedule C).

So, how does the IRS make the determination / re-determination? There’s no single test that automatically classifies an activity as one or the other. Instead, the IRS reviews a set of factors to decide whether the activity is a business or a hobby (see Treas. Reg. Sec. 1.183-2(b)):

- Manner in which the taxpayer carries on the activity (books & records, business, plan, advertising, etc.)

- Expertise of the taxpayer or their advisers (specialized workers, formal training / expertise, and general business experience)

- Time and effort spent by the taxpayer in carrying on the activity

- Expectation that the assets used in the activity may appreciate in value

- Success of the taxpayer in carrying on other similar or dissimilar activities

- Taxpayer’s history of income or loss with respect to the activity ( The IRS uses a “safe harbor” treating an activity as a business if it shows a profit in 3 of the last 5 years (2 of the last 7 years for breeding, training, or racing of horses). Taxpayers can elect not to have the presumption apply until the close of the fourth year of the activity (sixth year for horses) by filing Form 5213 Election to Postpone Determination as to Whether the Presumption Applies That An Activity Is Engaged in for Profit.)

- Amount of occasional profits earned, if any

- Financial status of the taxpayer

- Whether elements of personal pleasure or recreation are involved.

Its important to note that the Hobby Loss rules (IRC Sec. 183) applies to individuals, S corporations, estates, trusts, and partnerships. That being said, taxpayers may be able to avoid the loss limitations by operating the activity within a C corporation (Potter v. Commissioner).

Tips to help ensure your side hustle is treated as a business, and not a hobby, include doing the following:

- Keep detailed books and records: track all income, expenses, receipts, invoices. Document everything.

- Have a written business plan or profit strategy: show that you’re actively trying to make money. Perhaps market or advertise, adjust pricing, streamline costs, etc.

- Maintain a separate business bank/accounting structure – don’t commingle personal and business finances. Treat the side gig like a business entity.

- Show efforts to improve profitability – if you’re continually losing money but trying to change course (product, marketing, cost structure), it helps.

- If applicable: show expertise or seriousness – maybe relevant education/training, prior experience, or consultation with professionals.

Bottom line is the more “business-like” you are, the better your case will be, especially if the activity is losing money in early years or beyond the safe harbor. For example, incurring losses in 3 of the last 5 years vs profits.

In conclusion, If you aren’t sure whether you have business income or hobby income or if you are worried about being subject to hobby loss rules due to repeated losses, shoot us an email and we would be glad to help!

Disclaimer: The information provided herein is intended solely for informational purposes and no person(s) or other third-party may rely upon it as financial, tax, or legal advice or use it for any other purposes. As a result, Royal Financial, and any affiliates, assume no responsibility whatsoever to readers, or any other persons for that matter, as a result of the information contained herein.