⏱ Estimated reading time: 4 min read

By now, most taxpayers and practitioners have heard about the One Big Beautiful Bill Act that was signed into law on July 4, 2025.

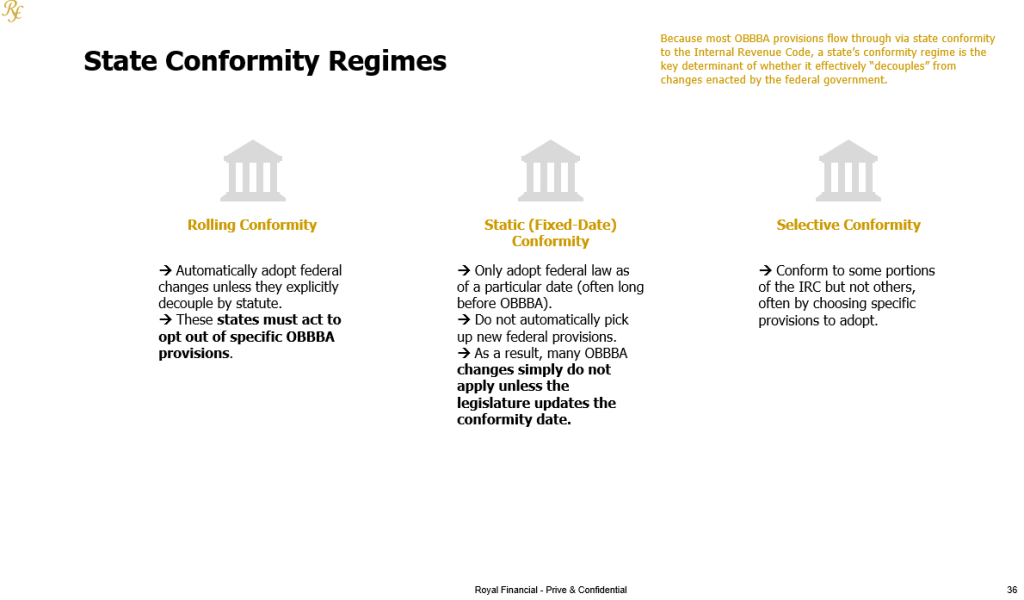

However, what’s often overlooked is the state tax implications of the OBBBA. States operate separately from the federal government so they don’t have to honor the changes enacted by the federal government. This is referred to as “decoupling”. When it comes to state tax legislation there are several conformity regimes utilized by states, listed below:

- Rolling Conformity -> Automatically adopt federal changes unless they explicitly decouple by statute. These states must act to opt out of specific OBBBA provisions.

- Static (Fixed-date) Conformity -> Only adopt federal law as of a particular date (often long before OBBBA). They do not automatically pick up new federal provisions. As a result, many OBBBA changes simply do not apply unless the legislature updates the conformity date.

- Selective Conformity -> Conform to some portions of the IRC but not others, often by choosing specific provisions to adopt.

Because most OBBBA provisions flow through via state conformity to the Internal Revenue Code, a state’s conformity regime is the key determinant of whether it effectively “decouples.”

Typical Areas of Decoupling

The top areas of decoupling, really come down to the largest revenue hits for each respective state. This generally encompasses the following provisions as they pertain to the OBBBA:

- Research & experimental (§174)

- Bonus depreciation (§168(k))

- Deduction for qualified production property (§168(n))

- Business interest expense limitation (§163(j))

- Qualified Tips (§224)

- Qualified Overtime (§225)

- SALT Cap Deduction (§164(b)(7))

With that in mind, here are examples of how specific states have responded as of December 2025:

- California -> Updated its IRC conformity date but specifically ensured the new date does not incorporate any OBBBA provisions, effectively decoupling.

- Michigan -> Decoupled from R&E (§174), bonus depreciation (§168(k)), deduction for qualified production property (§168(n)), and business interest expense limitation (§163(j)).

- Virginia -> A static conformity state, paused automatic conformity and required legislative action if revenue impact exceeds thresholds.

- Arizona -> Passed a bill to eliminate state income tax on tips for individual income tax purposes.

- North Carolina -> Proposed exempting tips, overtime, and some bonuses, though the bill had not passed by late 2025.

- New Jersey ->Introduced a bill to stop taxing all tip income, with no cap, specifically to help lower-income service workers.

- Colorado -> Decoupled from overtime deduction but allow the tips deduction.

State actions vary by tax type (corporate vs. individual), and some measures are temporary or proposed. With that said the environment is subject to change and you should do further diligence in the states in which you have nexus or plan to have nexus.

Conclusion

While the OBBBA introduced meaningful federal tax changes, it has also forced states to make critical conformity decisions that can significantly alter expected tax outcomes. These state-level responses are still developing, and many taxpayers may not realize they are impacted until returns are prepared.

If you are unsure how your state—or states—are treating OBBBA provisions such as bonus depreciation, R&E, tips, or overtime, I encourage you to email us directly. A brief conversation now can help avoid surprises later and identify planning opportunities before states finalize their positions.

Disclaimer: The information provided herein is intended solely for informational purposes and no person(s) or other third-party may rely upon it as financial, tax, or legal advice or use it for any other purposes. As a result, Royal Financial, and any affiliates, assume no responsibility whatsoever to readers, or any other persons for that matter, as a result of the information contained herein.