⏱ Estimated reading time: 2 min read

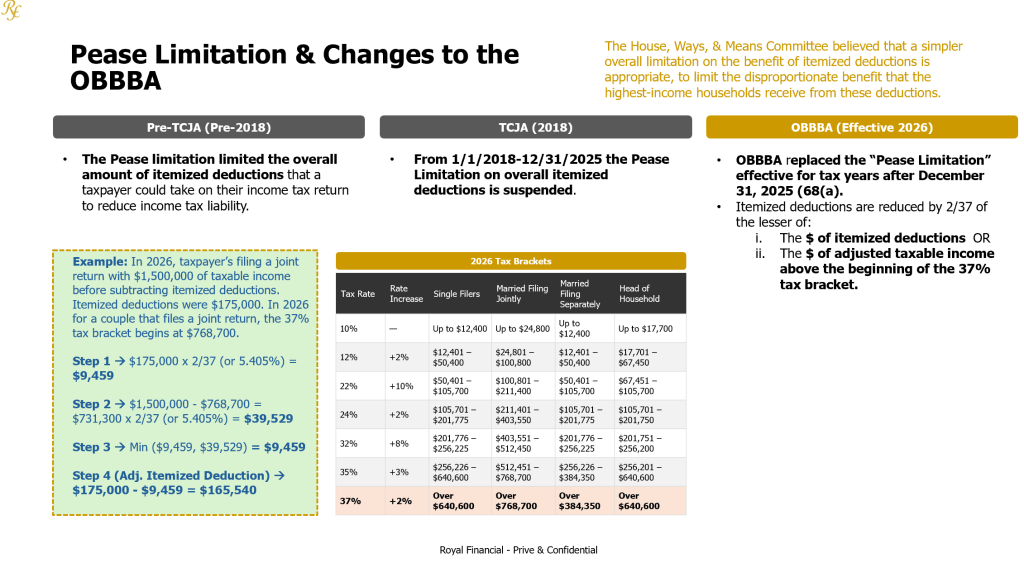

Under the Tax Cuts & Jobs Act (TJCA) the Pease limitation was suspended from 2018 – 2025. The Pease Limitation applied to high-income taxpayers and worked by reducing the value of a taxpayer’s itemized deductions by 3 percent for every dollar of taxable income above a certain threshold ($261,500 single; $313,800 married in 2017).

In July 2025, under the One Big Beautiful Bill Act (OBBBA), the Pease limitation was permanently replaced. Instead of reducing deductions based on AGI, the new rule limits deductions by reference to the top marginal tax bracket (37%). See the slide below summarizing the changes.

Why this matters for high-net worth individuals and high-income earners?

While the percentage haircut may look modest at first glance, the impact can be significant depending on your tax profile. The limitation applies every year starting in 2026 and It affects all itemized deductions collectively.

Planning Considerations

Given this change, the last week of 2025 presents a final planning window for accelerating deductions & planning for 2026.

Conclusion

For taxpayers consistently above the top bracket threshold, the difference between deducting expenses in 2025 vs. 2026 can be meaningful. If you need help help estimating the impact of the OBBBA on your itemized deductions, send us an email ASAP.

Disclaimer: The information provided herein is intended solely for informational purposes and no person(s) or other third-party may rely upon it as financial, tax, or legal advice or use it for any other purposes. As a result, Royal Financial, and any affiliates, assume no responsibility whatsoever to readers, or any other persons for that matter, as a result of the information contained herein.