⏱ Estimated reading time: 6 min read

After years of rapid home price appreciation, many homeowners are now sitting on significant unrealized gains. Even with higher interest rates slowing transaction volume, values in many markets remain well above pre-pandemic levels.

For homeowners who purchased years ago a sale today can easily trigger gains that exceed the $250,000 or $500,000 exclusion thresholds. That makes understanding the rules under IRC §121 more important than ever.

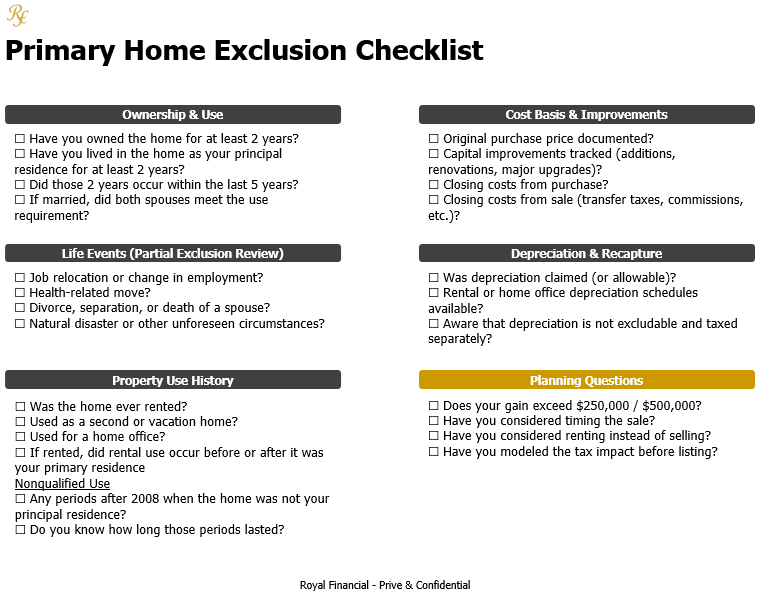

IRC §121 provides an exclusion of gain from sale or exchange of a principal residence. In order to qualify the taxpayer must meet ownership & use tests during the five-year period ending on the date of sale. Ownership & use tests do not have to be concurrent.

- Ownership Test -> Owned the home for at least 2 years, and

- Use Test -> Used the home as a principal residence for at least 2 years

Meet the test, and most — but not always all — of the gain may be excluded.

Why this matters now?

In a slower transaction environment, homeowners are often:

- Holding properties longer than originally planned

- Converting former residences into rentals

- Moving due to employment or family changes after long appreciation cycles

The result? A growing number of sellers are discovering that:

- Their gain exceeds the standard exclusion

- Part of the gain is taxable due to nonqualified use or

- Depreciation recapture creates tax even when the main gain is excluded

These issues tend to surface late in the process, often after a sale contract is already signed.

The Partial Exclusion

Taxpayers who don’t meet the full 2 out of 5-year requirement may still qualify for a partial exclusion if the sale is primarily due to:

- A change in employment

- Health-related reasons or

- Unforeseen circumstances

Common triggers in practice include certain natural disasters or involuntary conversions, job relocations, divorce or separation, or death of a spouse. The exclusion is pro-rata based on time of qualifying use.

Partial Exclusion Example: A single taxpayer resides in a home for 12 months and then sells the property due to a qualifying job relocation.

– Maximum exclusion:$250,000

– Ownership and use requirement met: 12 ÷ 24 months = 50%

– Allowed exclusion: $250,000 × 50% = $125,000

In high-appreciation markets, even a **partial exclusion** can significantly reduce—or fully eliminate—a sizable tax liability.

Nonqualified Use (Post-2008)

If after 2008 you, or your spouse or former spouse, didn’t use your home as a principal residence, this type of usage may affect your gain or loss calculations. In specific, the gain must be allocated between Qualified Use & Nonqualified Use. Nonqualified use generally includes periods after 2008 when the property was rented out, used as a second or vacation home, or was otherwise not used as a principal residence.

✅ Protected Activities

- Live in home first → move out → sell later

- Live in home first → rent briefly → sell later

- Live in home first → leave vacant → sell later

❌ Unprotected Activities

- Rent the home before ever living in it

- Use as a second/vacation home before principal residence use

- Convert to rental long before it was ever a primary residence

Planning Note: Nonqualified use is primarily a problem when a home is used as a rental or second home before it was ever a primary residence, not when a homeowner simply moves out and waits to sell.

Impact of Depreciation Recapture

In today’s market, depreciation recapture is one of the most common surprises when selling a home. Recapture applies to depreciation taken after May 6, 1997. Even though recapture on real property is limited to a 25% tax rate, it can still end up being quite the surprise on a taxpayer’s tax return if they were expecting little to no tax.

Below is an example, directly from Treas. Reg. §1.121-1(d)(2):

Example: On July 1, 1999, Taxpayer A moves into a house that he owns and had rented to tenants since July 1, 1997. A took depreciation deductions totaling $14,000 for the period that he rented the property. After using the residence as his principal residence for 2 full years, A sells the property on August 1, 2001. A’s gain realized from the sale is $40,000. A has no other section 1231 or capital gains or losses for 2001. Only $26,000 ($40,000 gain realized—$14,000 depreciation deductions) may be excluded under section 121. Under section 121(d)(6) and paragraph (d)(1) of this section, A must recognize $14,000 of the gain as unrecaptured section 1250 gain within the meaning of section 1(h).

Do you need to sell?

In some cases, taxpayers with very large unrealized gains may consider delaying a sale altogether by using an installment sale or converting the primary residence into a rental property. While these strategies don’t eliminate tax, they offer the ability to defer taxable income into lower income-tax years.

Planning Note: If you sell a home and your gain exceeds the §121 exclusion, that excess gain is generally still capital gain (usually long-term capital gain if you owned it > 1 year). It’s not automatically taxed at your ordinary income tax rate (e.g., 37%). This means the primary benefit of this approach is often deferral rather than a lower tax rate.

Planning Before You Sell Matters More Than Ever

When home values were modest, these rules often didn’t matter. Today, with many homeowners sitting on six-figure (or larger) gains, small missteps can translate into real tax dollars.

A proactive review can help:

- Maximize available exclusions

- Identify partial exclusion opportunities

- Review cost-basis (purchase price, additions, improvements, transaction costs, etc.)

- Quantify depreciation recapture early

- Avoid surprises at closing or tax time

Conclusion

The primary residence exclusion remains one of the most valuable tax benefits available to individuals, but in today’s real estate market, it’s no longer “automatic.” If you’re considering selling a home, especially one that has been rented, partially used for business, or held for many years, advance planning is critical. If you have questions or want help modeling the tax impact of a potential sale send us an email.

Disclaimer: The information provided herein is intended solely for informational purposes and no person(s) or other third-party may rely upon it as financial, tax, or legal advice or use it for any other purposes. As a result, Royal Financial, and any affiliates, assume no responsibility whatsoever to readers, or any other persons for that matter, as a result of the information contained herein.